“We want to make humanity a space-faring civilization. Take humanity to Mars, the Moon, and ultimately beyond,” said Elon, sharing his Mission Statement, the SpaceX roadshow accelerating to ludicrous speed. “Starship V3 is aiming for 100 tons to orbit with full reusability. Starship V4 we’re aiming for over 200 tons per mission and being able to launch every hour,” he said. “The propellant is liquid oxygen and liquid methane, which is the cheapest propellant you could possibly get. Which means that you should be able to send cargo to space for less than the cost of cargo on an airplane going on a trans-oceanic trip.”

Overall: “It’s increasingly difficult to build power plants on the ground - very few people want one in their backyard,” said Elon Musk, describing one of a multitude of constraints separating humanity from its infinite potential. “If you wanted to double US electricity usage, you’d have to build twice as many power plants, and most communities aren’t excited about that. But if we go to space, we can go far beyond Earth’s electricity generation,” he continued. “You could increase human energy by a factor of a million and still be using much less than a millionth of the sun’s energy. Current human civilization uses much less than a trillionth of the sun’s energy.” Humanity remains at 0 on the Kardashev Scale, still crawling slowly out from the primordial darkness. “It’s humbling how tiny we are.” A mote of dust suspended in a sunbeam. “You can manufacture solar radiators on the Moon from lunar materials. We could probably do around 1 terawatt per year of AI space compute from Earth, but 1,000 terawatts or more from the Moon – a truly staggering number.” Humanity currently consumes just 3.5 terawatts of electricity. So 1,000 terawatts of annual expansion is roughly 285x current consumption. “A limiting factor we see is being able to make chips - both logic, memory, and packaging. There’s not a single high-volume computer memory fab in America right now. Zero. One is being built in Idaho by Micron but won’t reach volume until ~2028, and the New York one is 2029–2030,” he said, listing another severe constraint. “This is a tiny fraction of the memory needed. Even under the best-case assumptions of existing fabricators, it’s not enough to meet anticipated AI demand. That’s why we need to do the Terafab.” Current global fabrication capacity is only producing roughly 2% of what Musk claims his companies will ultimately need for AI, robotics, and space infrastructure. “We want to make science fiction real, go to places that have never been explored before. You know, like, make Star Trek real.”

For Week-in-Review and Weekly & Year-to-Date market data, scroll to the bottom.

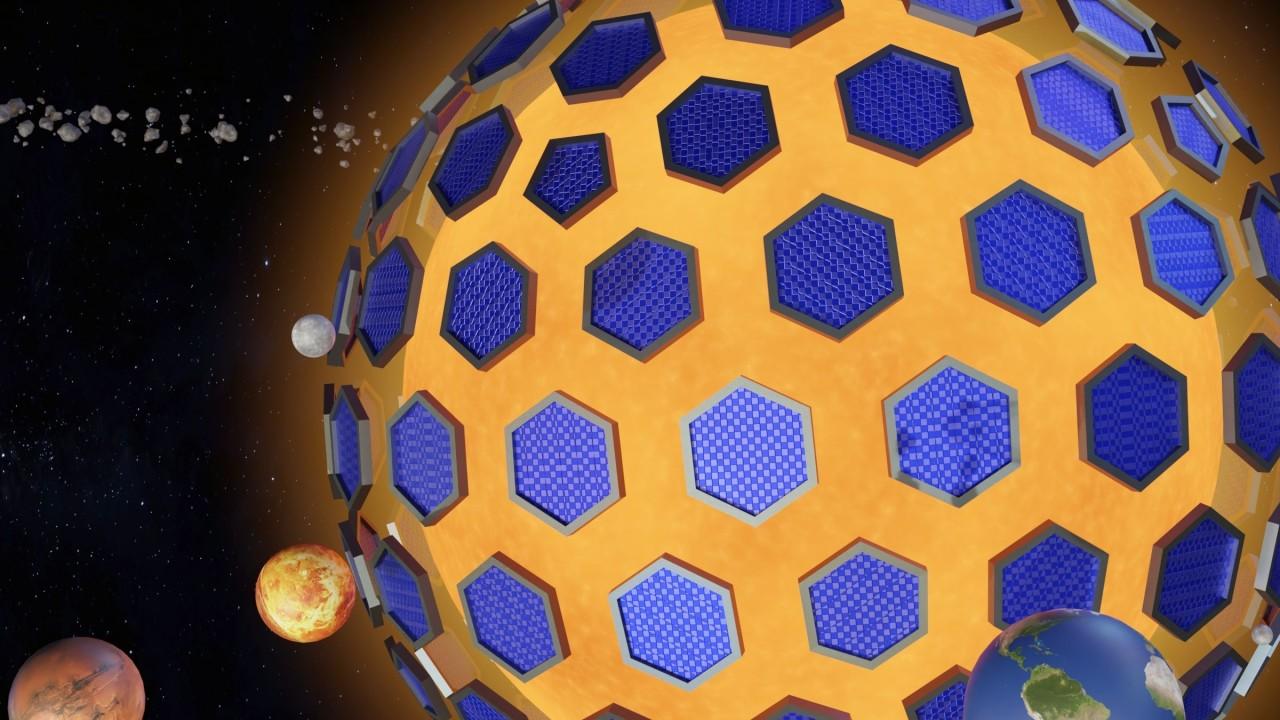

Dyson Sphere: In 1964, well before we could imagine the energy required to power today’s AI infrastructure, Soviet astronomer and visionary Nikolai Kardashev proposed a scale to measure civilizations in a paper on searching for extraterrestrial intelligence. The idea was that more advanced civilizations would need to harness vastly more energy, making energy consumption a universal proxy for technological progress. Kardashev defined three civilization types. Type I, Type II, and Type III. Humanity has not yet climbed onto the scale; we remain Type 0.

Dyson Sphere II: A Type I civilization can harness and store all the energy available on its home planet, including incoming stellar energy (e.g., total solar radiation hitting Earth), geothermal, wind, etc. It has full control over planetary resources and weather/climate. A Type II civilization can capture and use the entire energy output of its star. This involves megastructures like the Dyson Sphere - a vast array of solar collectors orbiting a star. A Type III can harness the energy of an entire galaxy, tapping into the output of billions of stars, black holes, and other sources.

Dyson Sphere III: In our 300,000-year ascent, Homo sapiens have gone from using a trace amount of Earth’s available energy to currently harnessing roughly 0.1–0.2% of the energy required for a full Type I Kardashev civilization. Reaching Type I would require planetary-scale engineering (e.g., massive solar arrays, fusion at enormous scale, climate/weather control, or space-based power). Simply burning 500× more fossil fuels isn’t feasible or desirable. Optimistic models (with sustained 3% growth or breakthroughs like fusion) project it in 100-200+ years.

Audacious: Earth formed, 4.54bln years ago. Platinum sank to its center. 300mm years later, as Earth’s crust was forming, an impact ejected what is now the moon. For the next few hundred million years, meteorites rained down, depositing 99% of the platinum now found in Earth’s crust. 40,000 near-earth asteroids are known, a far smaller number are mining targets. A single small high-grade asteroid can contain far more accessible platinum than has ever been mined on Earth. There is one known asteroid estimated to have $10,000 quadrillion of mineable metals.

Audacious II: “It’s really hard to find people with the intelligence, skills, and experience to do what we’re attempting here,” admitted the engineer, giving my daughter Liv and me a tour of his start-up; an asteroid mining company. I’d asked what some of his less obvious constraints were. His whole mission is so ambitious. But launch costs are collapsing along an exponential curve, plus, his satellite development costs are a fraction of the aerospace majors. “And on top of that, we need these people to be insane enough to devote their careers to a mission this audacious.”

Anecdote: “Pretty sure that’s 29 Palms down there,” said Liv, glued to the window, the two of us flying to Aerospace Alley. A vast wasteland spread 35,000 feet below us. 29 Palms is the US Marine Corps’ largest base, 1,100 square miles of high Mojave Desert, bigger than Rhode Island. If energy was abundant and nearly free, 29 Palms could be transformed into an irrigated oasis. Or a lush jungle. Cropland. Even a winter wonderland. The Mojave Desert could become anything we want. When I fly over the world’s most desolate places, I imagine the untapped potential of our planet. From the time Prometheus stole fire from Zeus and gave it to humans, our rise has moved in rough lockstep with energy consumption. Everything in the universe is energy of course. E=MC2. But we have yet to solve the riddle of harnessing this ubiquitous resource at Kardashev scale. If we fail to move beyond burning fossils, mankind will inevitably succumb to scarcity and eat itself alive in a hellscape like 29 Palms. But if we solve the riddle, utopia awaits, a flourishing, expansion. Everything becomes possible with limitless energy. And yet, only when we face hard constraints does humanity find a way. For 50yrs we have managed to skirt real constraints, creating roughly 2.1% more energy globally each year and building infrastructure to accommodate this incremental growth. That unambitious era is now over. The existential race toward AGI and then ASI will require far more energy than any of us can quite comprehend – a quantum leap in demand that the status quo cannot possibly satisfy. This race has produced a hard constraint of our own creation. And irrespective of what our LLMs ultimately yield, the next stage of humanity’s inexorable advance is beginning, with a competition to harness energy in ways and at scales previously unimaginable to all but our greatest visionaries.

Good luck out there,

Eric Peters

Chief Investment Officer

One River Asset Management

Week-in-Review: Mon: US ISM mfg 54.0 (53.0e). Eurozone unemp rate 6.3% (6.2%e), M3 money supply 2.7% (3.1%e). India IP 4.9% (3.9%e). South Korea CPI 3.1% (2.9%e). Anthropic pulled ahead of OpenAI with a confidential IPO filing, as the two AI startups battle for a fundraising edge. S&P +0.3%. Tue: US JOLTS job openings 7,618k (6,866k e). Poland base rate unch 3.75% as exp. Eurozone CPI 3.2% as exp, Core 2.5% (2.4%e). Australia GDP 2.5% (2.6%e). A surprise approval by the US Commerce Department paves the way for Chinese-controlled firms to enter the US vehicle market. US is proposing new tariffs of at least 10% on imports from 60 trading partners. US and Iran exchange strikes, putting fresh strain on ceasefire. S&P +0.1%. Wed: US ADP emp change 122k (120k e), durable goods orders 8.0% (7.9%e), factory orders 4.8% (4.6%e). Russia unemp rate 2.2% as exp. US says Israel, Lebanon agree to implement ceasefire. SpaceX seeks $75B in record IPO to fund AI, rocket launches, and satellite infrastructure. S&P -0.7%. Thu: US init jobless claims 225k (215k e), cont claims 1777k (1780k e). BOJ officials are set to consider June rate hike with another possible later this year. US-Iran talks progress stalls after Hezbollah rejects truce. S&P +0.4%. Fri: US unemp rate 4.3% as exp, change in nonfarm payrolls 172k (88k e). Canada unemp rate 6.6% (6.9%e). Eurozone GDP SA 0.3% (0.8%e). India RBI repurchase rate unch 5.25% as exp. US-Iran nears 100-day mark, remaining at odds over a potential truce, with Iran insisting on a ceasefire in southern Lebanon and the unfreezing of $24 billion in assets. S&P Dow Jones Indices’ index committee declined to remove a rule that companies generate positive net income for the past year to be included in the S&P 500 Index, a potential hurdle for SpaceX, Anthropic, and OpenAI inclusion. S&P -2.6%.

Weekly Close: S&P 500 -2.6% and VIX +6.19 at +21.51. Nikkei +0.4%, Shanghai -1.0%, Euro Stoxx -0.5%, Bovespa -2.7%, MSCI World +0.02%, MSCI Emerging +0.4%, Bitcoin -18.7%, and Ethereum -22.7%. USD rose +3.7% vs Russia, +2.7% vs Chile, +2.6% vs Brazil, +2.3% vs Sweden, +2.1% vs South Africa, +1.9% vs Australia, +1.2% vs Euro, +1.0% vs Canada, +0.9% vs Sterling, +0.8% vs Indonesia, +0.7% vs Mexico, +0.6% vs Yen, +0.4% vs Turkey, and +0.3% vs China. USD fell -0.1% vs India. Gold -5.0%, Silver -8.9%, Oil (WTI) +3.6%, Oil (Brent) +1.9%, NatGas (US) -1.9%, NatGas (EU) +5.4%, Power (EU) -0.8%, Copper -1.6%, Iron Ore -2.3%, Corn -6.5%. 10yr Inflation Breakevens (EU +2bps at 2.05%, US -4bps at 2.37%, JP +5bps at 2.24%, and UK -1bp at 3.32%). 2yr Notes +14bps at 4.15% and 10yr Notes +9bps at 4.53%.

Manufacturing PMI (high-to-low): Sweden 57.3 (previous month 57), Switzerland 57.3 (previous month 54.5), Taiwan 56.1 (previous mth 55.3), Netherlands 55.9/54.4, India 55/54.7, South Korea 54.8/53.6, Japan 54.5/55.1, US 54/52.7, UK 53.9/53.7, Greece 53.3/52.4, Canada 52.9/53.3, Italy 52.9/52.1, Vietnam 52.8/50.5, Czech Republic 52.2/52.9, China 51.8/52.2, Austria 51.7/51.2, Spain 51.2/51.7, Singapore 51/50.7, Hong Kong 50.4/48.6, Hungary 50.2/50.4, Germany 50.1/51.4, Indonesia 50/49.1, Turkey 49.8/45.7, France 49.7/52.8, Mexico 49.6/47.7, South Africa 49.6/51.6, Poland 49.4/48.8, Brazil 49.1/52.6. Services PMI: India 59.8/58.8, China 54.4/52.6, Sweden 53.9/52.6, Ireland 50.8/49.7, US 50.7/51, Brazil 50.4/52.3, Spain 50.1/47.9, Japan 50/51, Italy 49.4/49.8, UK 49.3/52.7, Russia 48.7/49.7, Australia 48.7/50.7, Germany 48.1/46.9, France 44.3/46.5.

YTD Equity Index Returns: Korea +79.1% price in US dollars (+93.6% priced in won), Taiwan +55.2% priced in US dollars (+55.6% priced in Taiwan dollars), Norway +30.1% in US dollars (+22% in krone), Japan +29% in dollars (+32.3% in yen), Hungary +28.1% (+20.4%), Israel +25.1% (+15.5%), Thailand +20.3% (+25.6%), Russell 2000 +14.2%, Turkey +13.4% (+21.6%), Finland +12.6% (+14.8%), Poland +12.1% (+14.9%), Austria +12.1% (+14.2%), Brazil +11.9% (+4.9%), Colombia +11.6% (+6%), NASDAQ +10.6%, Portugal +10.4% (+12.3%), MSCI World +9.8% priced in US dollars, Greece +9.1% (+11.1%), Italy +8.9% (+11%), Singapore +8.4% (+8.7%), Belgium +8% (+9.9%), S&P 500 +7.9%, Netherlands +7.5% (+9.4%), Canada +6.8% (+8.5%), Mexico +6% (+2.9%), Sweden +5.1% (+8.1%), Australia +4.7% (-1%), Saudi Arabia +4.6% (+4.8%), China +4.5% (+1.5%), Spain +4.1% (+6%), UK +3.7% (+4.4%), Vietnam +2.9% (+3%), Euro Stoxx 50 +2.9% (+4.7%), Argentina +1.8% (+1.1%), Malaysia +1.5% (+0.8%), Switzerland +0.4% (+0.9%), Germany -0.8% (+1.1%), France -0.9% (+0.8%), Ireland -1.6% (+0.1%), New Zealand -1.9% (-2.9%), HK -3.2% (-2.6%), Chile -3.6% (-2%), UAE -3.8% (-3.8%), South Africa -4.1% (-4.2%), Philippines -6.7% (-1.9%), Denmark -6.9% (-5.7%), Czech Republic -7.6% (-5.9%), India -15.7% (-10.6%), Indonesia -40.3% (-35.3%).

Disclaimer: All characters and events contained herein are entirely fictional. Even those things that appear based on real people and actual events are products of the author’s imagination. Any similarity is merely coincidental. The numbers are unreliable. The statistics too. Consequently, this message does not contain any investment recommendation, advice, or solicitation of any sort for any product, fund or service. The views expressed are strictly those of the author, even if often times they are not actually views held by the author, or directly contradict those views genuinely held by the author. And the views may certainly differ from those of any firm or person that the author may advise, converse with, or otherwise be associated with. Lastly, any inappropriate language, innuendo or dark humor contained herein is not specifically intended to offend the reader. And besides, nothing could possibly be more offensive than the real-life actions of the inept policy makers, corrupt elected leaders and short, paranoid dictators who infest our little planet. Yet we suffer their indignities every day. Oh yeah, past performance is not indicative of future returns.